Introduction to GAUSS for EViews Users#

This guide helps EViews users do the same things in GAUSS. If you’re comfortable with workfiles, VAR models, IRFs, and ARIMA estimation, you’ll find equivalent tools in GAUSS – with more flexibility for custom models and reproducible workflows.

Note

This guide is written for GAUSS 26. Time series functions (ARIMA, VAR, GARCH) require the TSMT add-on.

How GAUSS Differs from EViews#

Your analysis is code. EViews blends GUI dialogs, command window entries, and program files. In GAUSS, your entire workflow is a program file – reproducible, version-controlled, and shareable. No clicking through dialogs to re-estimate.

No workfile – load data directly. EViews requires creating a workfile first, then importing series into it. GAUSS loads data directly into a dataframe with

loadd()– no workfile setup step.Multiple datasets at once. EViews ties your analysis to one workfile at a time. GAUSS can hold many datasets in memory simultaneously.

Results in structures, not object views. EViews stores results in “equation” and “VAR” objects that you view in windows. GAUSS returns results in structures with named members (

out.b,out.sigma) that you access in code.Full programming language. EViews handles loops and basic logic. GAUSS is a complete matrix programming language – you can write custom estimators, simulation studies, and bootstrap procedures.

Where to type code:

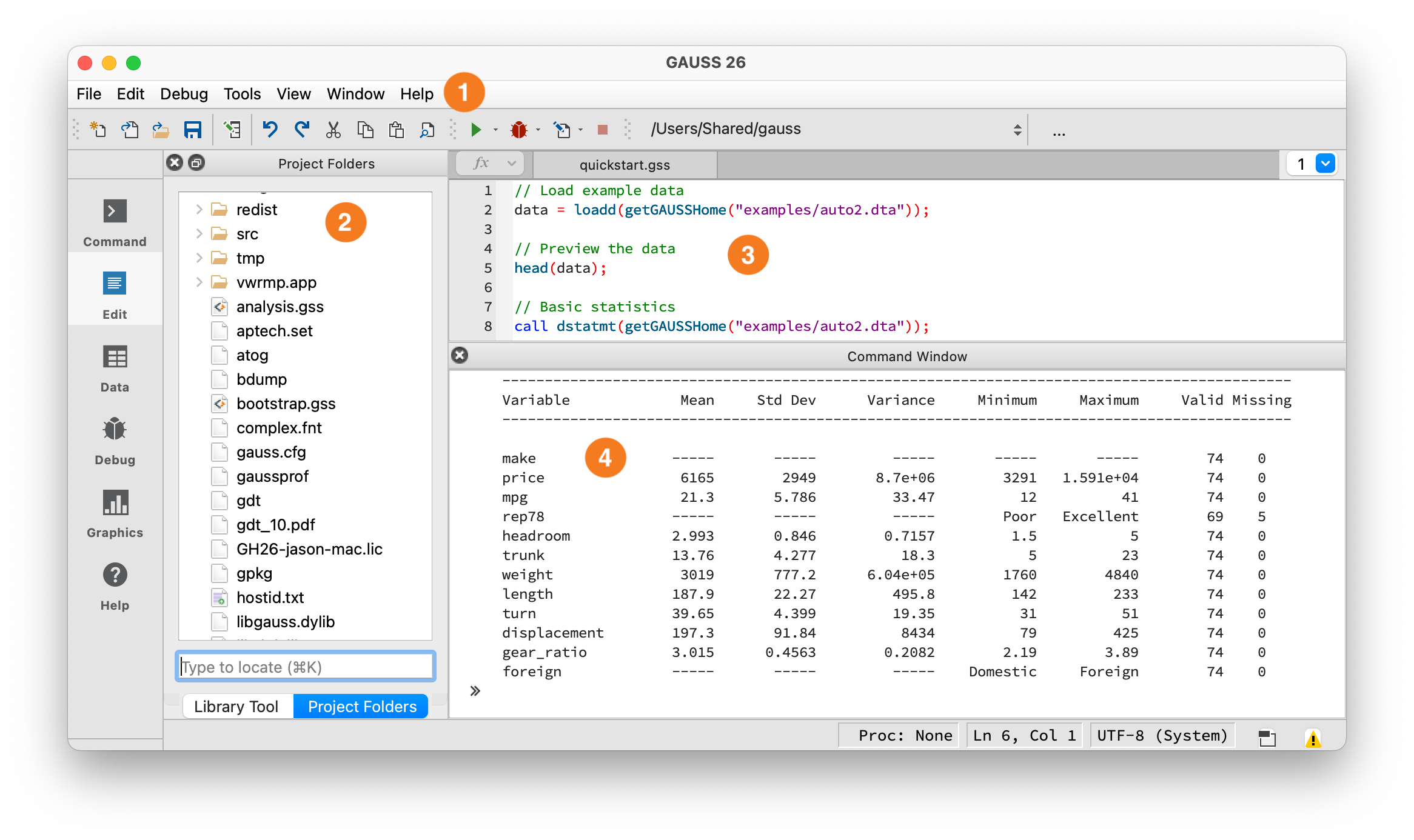

The GAUSS IDE workspace.#

① Toolbar — Shows your current working directory and the Run button (green arrow). Click it or press F5 to execute. ② Project Folders — File browser, similar to EViews’ Workfile contents. ③ Editor — Write programs here, similar to EViews’ program editor. ④ Command Window — Output appears here, similar to EViews’ output window. You can also type single lines at the >> prompt.

Debugging: Errors appear in the Output window with a line number – click it to jump to the error. Use the Variables panel (View > Variables) to inspect values at runtime. You can set breakpoints by clicking in the left margin of the editor, then step through code with the Debug menu. For quick debugging, insert print varname; statements.

Key Syntax Differences#

Feature |

EViews |

GAUSS |

|---|---|---|

Statement end |

Newline |

Required |

Indexing |

1-based (series obs) |

1-based |

String quotes |

|

|

Assignment |

|

|

All rows/cols |

(implicit in series) |

|

Comments |

|

|

String concat |

|

|

String equality |

|

|

Operators#

Matrix vs element-wise multiplication:

// GAUSS

A * B; // Matrix multiplication

A .* B; // Element-wise multiplication

A .^ 2; // Element-wise power

A ./ B; // Element-wise division

A'; // Transpose

Warning

``*`` is matrix multiplication in GAUSS. EViews handles this behind the scenes. In GAUSS, A * B is matrix multiplication and A .* B is element-wise. Using the wrong one produces wrong results silently.

Comparison operators have two forms. Without a dot, A > 0 returns a scalar – true only if ALL elements satisfy the condition. With a dot, A .> 0 tests each element individually:

// GAUSS

A .> 0; // Element-wise: returns 1/0 for each element

A .== B; // Element-wise equality

A .and B; // Element-wise AND

A .or B; // Element-wise OR

Warning

A > 0 is true only if every element is positive (like EViews’s @all). A .> 0 tests each element. Both forms exist for: >/.>, </.<, >=/.>=, <=/.<=, ==/.==, !=/.!=.

Concatenation#

// GAUSS

A ~ B; // Horizontal concatenation (tilde)

A | B; // Vertical concatenation (pipe)

a $+ b; // String concatenation

Warning

``|`` is vertical concatenation, not logical OR. condition1 | condition2 stacks two vectors vertically. Use .or for logical OR and .and for logical AND.

For string arrays, use $~ (horizontal) and $| (vertical): "Domestic" $| "Foreign" creates a 2x1 string array.

String operators use the ``$`` prefix. In EViews, + concatenates strings and = compares them. In GAUSS: $+ (concatenation), $== (equality), $~ (horizontal join), $| (vertical join).

Indexing#

EViews manages series by name within a workfile. In GAUSS, you index dataframes directly by row and column:

// GAUSS

data = loadd("gdp_data.xlsx");

data[., "gdp"]; // Column by name (dot = all rows)

data[., "gdp" "cpi"]; // Multiple columns (space-separated names)

data[., 1]; // Column by position

data[1, 1]; // First row, first column

data[1:10, .]; // Rows 1 through 10 (inclusive)

data[rows(data), .]; // Last row (no negative indexing)

Key points:

GAUSS uses

.for “all rows” or “all columns”Slices are inclusive:

data[1:5, .]gets rows 1 through 5No negative indexing. Use

rows(data)for the last row.

Note

Most examples below use the auto2 dataset bundled with GAUSS. To run them, load it first:

auto2 = loadd(getGAUSSHome("examples/auto2.dta"));

Data: Workfiles vs. Dataframes#

In EViews, you create a workfile and import series:

' EViews

wfcreate q 1960Q1 2020Q4

import "gdp_data.xlsx"

In GAUSS, you load data directly into a dataframe – no workfile setup:

// GAUSS - one function reads CSV, Excel, Stata, SAS, SPSS, HDF5

data = loadd("gdp_data.xlsx");

// Check what you loaded

print getcolnames(data)'; // Column names

print rows(data) "observations";

head(data); // First 5 rows (like EViews's spreadsheet view)

Loading specific variables uses a formula string with +:

// Load only these variables

data = loadd("macro_data.csv", "gdp + cpi + unrate");

// Load all variables except one

data = loadd("macro_data.csv", ". -date_str");

Accessing variables:

' EViews - reference by name

show gdp

// GAUSS - index by column name

gdp = data[., "gdp"];

Creating new variables:

' EViews

series gdp_growth = dlog(gdp)

series lgdp = log(gdp)

// GAUSS - use lagn() for lags, ln() for natural log

lgdp = ln(data[., "gdp"]);

gdp_growth = lgdp - lagn(lgdp, 1); // lagn fills the first obs with missing

Warning

log vs ln: EViews’s log() is the natural logarithm. GAUSS’s log() is base 10. Use ln() in GAUSS. Forgetting this will silently corrupt every model that uses logged variables.

Generating lags and differences:

' EViews

series y_lag1 = y(-1)

series y_lag2 = y(-2)

series dy = d(y)

// GAUSS

y_lag1 = lagn(y, 1); // Lag 1 (first obs becomes missing)

y_lag2 = lagn(y, 2); // Lag 2 (first two obs become missing)

dy = y - lagn(y, 1); // First difference

dlog_y = ln(y) - lagn(ln(y), 1); // Log difference (like EViews's dlog)

Data Import/Export#

// GAUSS - loadd handles all formats

data = loadd("data.csv");

data = loadd("data.dta"); // Stata

data = loadd("data.sas7bdat"); // SAS

data = loadd("data.xlsx"); // Excel

// Export

saved(data, "output.csv");

saved(data, "output.xlsx");

Formula string quick reference: GAUSS uses formula strings in several contexts:

Data Manipulation#

' EViews

smpl if foreign = 0

sort mpg

// GAUSS

domestic = selif(auto2, auto2[., "foreign"] .== 0); // Filter rows

sorted = sortc(auto2, "mpg"); // Sort by column

Warning

GAUSS does not support boolean indexing. Use selif() to filter rows: selif(df, condition). Passing a boolean vector to brackets will not filter – it interprets the 0s and 1s as row numbers.

Common operations:

EViews |

GAUSS |

|---|---|

|

|

|

|

|

|

|

|

(manual in EViews) |

|

Missing Values#

EViews handles missing values within the workfile automatically. In GAUSS, you manage them explicitly:

' EViews

series y_clean = @nan(y, 0)

smpl if y <> NA

// GAUSS

miss(); // Creates a missing value (like EViews's NA)

ismiss(x); // Returns 1 if ANY element is missing (scalar)

x .== miss(); // Element-wise check (returns 1/0 vector)

packr(data); // Drop rows with any missing value

missrv(x, 0); // Replace missing with 0

Warning

ismiss is NOT element-wise. ismiss(x) returns a scalar (1 if any element is missing, 0 otherwise). For element-wise missing detection, use x .== miss().

Descriptive Statistics#

' EViews

gdp.stats

// GAUSS - dstatmt prints a summary table (like EViews's stats view)

call dstatmt(auto2[., "price" "mpg" "weight"]);

Output:

------------------------------------------------------------------------------------------

Variable Mean Std Dev Variance Minimum Maximum Valid Missing

------------------------------------------------------------------------------------------

price 6165.26 2949.50 8699530.9 3291 15906 74 0

mpg 21.30 5.79 33.47 12 41 74 0

weight 3019.46 777.19 604021.4 1760 4840 74 0

Column-wise statistics:

// GAUSS

meanc(x); // Column mean (the 'c' suffix = column-wise)

stdc(x); // Column standard deviation (uses N-1)

sumc(x); // Column sum

minc(x); // Column min

maxc(x); // Column max

median(x); // Median

// Row-wise

meanr(X); // Row mean (the 'r' suffix = row-wise)

sumr(X); // Row sum

OLS Regression#

' EViews

equation eq1.ls price c mpg weight

// GAUSS - print formatted summary (like EViews's equation view)

call olsmt(auto2, "price ~ mpg + weight");

Output:

Valid cases: 74 Dependent variable: price

Missing cases: 0 Deletion method: None

Total SS: 634007042 Degrees of freedom: 71

R-squared: 0.2926 Rbar-squared: 0.2727

Residual SS: 448544672 Std error of est: 2514.3269

F(2,71): 14.6874 Probability of F: 0.0000

Standard Prob Standardized Cor with

Variable Estimate Error t-value >|t| Estimate Dep Var

-------------------------------------------------------------------------------

CONSTANT 1946.069 3597.0496 0.54101 0.5902 --- ---

mpg -49.5122 86.1560 -0.57464 0.5674 -0.09717 -0.4559

weight 1.7466 0.3712 4.70402 0.0000 0.46030 0.5386

Tip

Use call olsmt(...) to print a formatted summary without saving results. The call keyword discards return values – useful for quick exploration.

Accessing results:

' EViews

eq1.@coefs

eq1.@se

eq1.@r2

// GAUSS

struct olsmtOut out;

out = olsmt(auto2, "price ~ mpg + weight");

print out.b; // Coefficient estimates

print out.stderr; // Standard errors

print out.rsq; // R-squared

print out.resid; // Residuals

print out.vc; // Variance-covariance of estimates

Key olsmtOut members: b (coefficients), stderr (standard errors), vc (variance-covariance matrix), rsq (R-squared), resid (residuals), dwstat (Durbin-Watson), sigma (residual std dev).

Time Series Analysis (TSMT)#

GAUSS’s time series tools are in the TSMT add-on. Add this line at the top of your script:

library tsmt;

If this produces an error, contact Aptech to add TSMT to your license. All examples in this section require TSMT.

ARIMA#

' EViews

equation eq1.ls d(gdp) c ar(1) ma(1)

// GAUSS

library tsmt;

// Load unemployment rate data

data = loadd(getGAUSSHome("examples/UNRATE.csv"));

y = data[., "UNRATE"];

// Fit ARIMA(1,1,1)

struct arimamtOut aOut;

aOut = arimaFit(y, 1, 1, 1);

Output:

================================================================================

Coefficient Estimate Std. Err. T-Ratio Prob |>| t

================================================================================

AR[1,1] -0.722 0.167 -4.333 0.000

MA[1,1] -0.798 0.143 -5.580 0.000

Constant -0.001 0.695 -0.001 0.999

================================================================================

VAR Estimation#

' EViews

var myvar.ls 1 2 dln_inv dln_inc dln_consump

// GAUSS

library tsmt;

// Load Lutkepohl data (included with TSMT)

data = loadd(getGAUSSHome("pkgs/tsmt/examples/lutkepohl2.gdat"));

// Select variables and estimate VAR

y = data[., "dln_inv" "dln_inc" "dln_consump"];

struct svarOut sout;

sout = svarFit(y);

Accessing VAR results:

' EViews

myvar.@coefs

myvar.@residcov

// GAUSS - results stored in structure members

print sout.coefficients; // Coefficient matrix

print sout.residuals; // Residuals

print sout.aic; // Information criteria

print sout.sbc;

Impulse Response Functions#

' EViews

myvar.impulse(10, a, m) dln_inv dln_inc dln_consump

// GAUSS - IRF computed as part of svarFit, just plot it

plotIRF(sout);

// Access the IRF matrices directly

print sout.irf;

Forecast Error Variance Decomposition#

' EViews

myvar.decomp(10) dln_inv dln_inc dln_consump

// GAUSS

plotFEVD(sout); // Plot variance decomposition

// Historical decomposition

plotHD(sout);

GARCH#

' EViews

equation eq1.arch(1,1) y c

// GAUSS

library tsmt;

y = loadd(getGAUSSHome("pkgs/tsmt/examples/garch.dat"));

struct garchEstimation gOut;

gOut = garchFit(y, 1, 1);

Output:

================================================================================

Model: GARCH(1,1) Dependent variable: Y

Time Span: Unknown Valid cases: 300

================================================================================

Coefficient Upper CI Lower CI

beta0[1,1] 0.01208 -0.00351 0.02768

garch[1,1] 0.15215 -0.46226 0.76655

arch[1,1] 0.18499 0.01761 0.35236

omega[1,1] 0.01429 0.00182 0.02675

================================================================================

AIC: 315.54085

LRS: 307.54085

For GJR-GARCH (asymmetric), use garchGJRFit(). For IGARCH, use igarchFit().

Unit Root Tests#

' EViews

y.uroot(adf, 4)

y.uroot(kpss)

// GAUSS (TSMT)

library tsmt;

// DF-GLS test (Elliott, Rothenberg, Stock 1996)

{ tstat, crit } = dfgls(y, 4); // max 4 lags

// KPSS stationarity test

{ tstat, crit } = kpss(y, 4); // max 4 lags

TSMT includes dfgls() (DF-GLS), kpss() (KPSS stationarity test), and the Zivot-Andrews structural break test. Results include test statistics and critical values at standard significance levels.

Forecasting#

' EViews

myvar.forecast(e) 12

// GAUSS - forecast from a VARMA model

library tsmt;

// Estimate and forecast

struct varmamtOut vOut;

vOut = varmaFit(y, 2, 0); // VAR(2)

fcast = varmaPredict(vOut, y, 0, 12); // 12 periods ahead (y=data, 0=no exog)

Plotting#

EViews has rich graph objects. GAUSS’s graphics library covers the same ground:

// GAUSS

plotXY(x, y); // Line plot

plotScatter(x, y); // Scatter plot

plotHist(x, 20); // Histogram with 20 bins

plotBox(data, "val ~ group"); // Box plot

plotBar(labels, heights); // Bar chart

plotTS(1960, 4, data[., "gdp"]); // Time series plot (start year, frequency, data)

Customizing plots uses a plotControl structure – think of it as configuring chart options before drawing:

// Create a scatter plot with title and labels

struct plotControl myPlot;

myPlot = plotGetDefaults("scatter");

plotSetTitle(&myPlot, "MPG vs Weight");

plotSetXLabel(&myPlot, "Weight (lbs)");

plotSetYLabel(&myPlot, "Miles per gallon");

plotSetLegend(&myPlot, "Domestic" $| "Foreign");

plotScatter(myPlot, auto2[., "weight"], auto2[., "mpg"]);

Subplots and saving:

plotLayout(2, 1, 1); // 2 rows, 1 col, position 1

plotSave("plot.png", 640|480); // Save with size (width|height in pixels)

Functions and Procedures#

EViews subroutines are limited to basic operations. GAUSS has a full procedure system:

' EViews

subroutine my_func(scalar x, scalar y)

%result = x + y

endsub

// GAUSS

proc (1) = my_func(x, y);

local result;

result = x + y;

retp(result);

endp;

answer = my_func(3, 4); // answer = 7

Key points:

proc (n) =declares the number of return valueslocaldeclares variables scoped to this procedure (see warning below)retp()returns valuesendpends the procedureProcedures can be defined anywhere in the file – before or after the code that calls them

Multiple outputs:

proc (2) = stats(x);

local mn, sd;

mn = meanc(x);

sd = stdc(x);

retp(mn, sd);

endp;

{ my_mean, my_std } = stats(rndn(100, 1));

Warning

Variables are global by default. In GAUSS, you must declare variables with local inside proc or they become globals that persist after the procedure returns. Forgetting local creates hard-to-find bugs where procedures silently modify variables in the calling scope. Make it a habit to declare local for every variable inside a proc.

Control Flow#

' EViews

for !i = 1 to 10

' do something

next

if condition then

' do something

endif

// GAUSS

for i (1, 10, 1);

print i;

endfor;

if x > 0;

print "positive";

elseif x < 0;

print "negative";

else;

print "zero";

endif;

do while x > 0;

x = x - 1;

endo;

Note: GAUSS requires semicolons after control statements (if, for, else, etc.). Inside a proc, remember to declare loop variables with local.

Common Operations: Quick Reference#

Task |

EViews |

GAUSS |

|---|---|---|

Load file |

|

|

Natural log |

|

|

Log base 10 |

|

|

First difference |

|

|

Lag |

|

|

OLS |

|

|

ARIMA |

|

|

VAR |

|

|

GARCH(1,1) |

|

|

Unit root test |

|

|

Stationarity test |

|

|

IRF plot |

|

|

Descriptive stats |

|

|

Scatter plot |

|

|

Export |

|

|

Sort |

|

|

Filter |

|

|

Drop missing |

|

|

|

|

|

Comment |

|

|

Note

Reminder: EViews’s log() is natural log. GAUSS’s log() is base 10. Use ln(). See the full warning in the Data section above.

Common Gotchas#

Semicolons required. Every statement ends with

;. This is the first thing EViews users forget.log() is base 10, ln() is natural log. EViews’s

log= GAUSS’sln.Operators are explicit.

*is matrix multiply,.*is element-wise.>is a scalar test,.>is element-wise.``|`` is concatenation, not OR. Use

.orfor logical OR,.andfor AND.No boolean indexing.

df[condition, .]does not filter. Useselif(df, condition).Declare ``local`` in procedures. Without

local, variables leak to the global scope.String operators need ``$``. Use

$+for concatenation,$==for equality.The ``call`` keyword. Use

call functionName(...)to run a function and discard its return value. This is useful for printing summaries:call olsmt(data, "y ~ x1");prints without saving.No negative indexing. Use

rows(x)for the last row,cols(x)for the last column.

Putting It Together#

Here is a complete, runnable example that loads data, creates variables, plots, and runs a regression. Press F5 to run it.

// Load the auto2 dataset bundled with GAUSS

auto2 = loadd(getGAUSSHome("examples/auto2.dta"));

// Summary statistics

call dstatmt(auto2[., "price" "mpg" "weight"]);

// Keep only domestic cars

domestic = selif(auto2, auto2[., "foreign"] .== 0);

// Add a new variable

domestic = dfaddcol(domestic, "price_k", domestic[., "price"] ./ 1000);

// Scatter plot with title

struct plotControl myPlot;

myPlot = plotGetDefaults("scatter");

plotSetTitle(&myPlot, "Weight vs MPG (Domestic Cars)");

plotSetXLabel(&myPlot, "Weight (lbs)");

plotSetYLabel(&myPlot, "Miles per gallon");

plotScatter(myPlot, domestic[., "weight"], domestic[., "mpg"]);

// OLS regression: how does weight affect fuel efficiency?

struct olsmtOut out;

out = olsmt(domestic, "mpg ~ weight");

// Print key results

print "Coefficients:"; print out.b;

print "Standard errors:"; print out.stderr;

print "R-squared:"; print out.rsq;

What’s Next?#

GAUSS Quickstart – 10-minute introduction to GAUSS basics

Running Existing Code – If you inherited GAUSS code and need to get it running

Data Management – Loading, cleaning, and reshaping data

Textbook Examples – Worked examples from Greene (Econometric Analysis) and Brooks (Introductory Econometrics for Finance)

Command Reference – Browse all 1,000+ built-in functions

Econometrics blog – Fully worked examples covering regression, panel data, hypothesis testing, and more

Time series blog – ARIMA, VAR, GARCH, cointegration, and forecasting tutorials with complete code