Chapter 9: Calculating Principal Components#

Example: PCA with US Treasuries “by hand”#

This example demonstrates how to compute principal component analysis (PCA) to analyze US Treasury bills and bonds.

Getting Started#

To run this example on your own you will need to install the BrooksEconFinLib package. This package houses all examples and associated data.

How to#

Step One: Load the data#

To start, load the relevant variables from the dataset using loadd() and a formula string.

To replicate this example, we will load the following variables:

Date - Observation date.

GS3M - Market yield on 3 month US Treasury bill.

GS6M - Market yield on 6 month US Treasury bill.

GS1 - Market yield on 1 year US Treasury bond.

GS3 - Market yield on 3 year US Treasury bond.

GS5 - Market yield on 5 year US Treasury bond.

GS10 - Market yield on 10 year US Treasury bond.

// Create file name with full path

data_set = getGAUSSHome() $+ "pkgs/BrooksEcoFinLib/examples/fred90.dta";

// Load all variables from file

data = loadd(data_set);

// Preview first 5 rows

head(data);

Date GS3M GS6M GS1 GS3 GS5 GS10

1990-01-01 7.9000 7.9600 7.9200 8.1300 8.1200 8.2100

1990-02-01 8.0000 8.1200 8.1100 8.3900 8.4200 8.4700

1990-03-01 8.1700 8.2800 8.3500 8.6300 8.6000 8.5900

1990-04-01 8.0400 8.2700 8.4000 8.7800 8.7700 8.7900

1990-05-01 8.0100 8.1900 8.3200 8.6900 8.7400 8.7600

Further reading: Data management guide

Function reference: getgausshome(), head(), loadd()

Step Two: Normalize the variables#

We need to normalize the variables by subtracting the means from each variable and dividing by the standard deviation. We will break this into several lines of code so you can look at some of the intermediate calculations.

The return values from stdc() and meanc() will be 6x1 column vectors. For us to be able to perform the element-by-element subtraction between the six elements of mu and the corresponding columns of yields, we need mu to have the same number of columns as yields. That is why we transpose mu (and sd) on the line that creates yields_norm.

// Create a datframe that contains

// the yields, but not the 'Date' variable

yields = delcols(data, "Date");

// Compute the means and standard

// deviations for each variable

mu = meanc(yields);

sd = stdc(yields);

// Subtract the mean and divide by

// the standard deviation for each column

yields_norm = (yields - mu') ./ sd';

head(yields_norm);

GS3M GS6M GS1 GS3 GS5 GS10

2.1723 2.1100 2.0424 1.9457 1.8806 1.8754

2.2150 2.1773 2.1227 2.0582 2.0194 2.0114

2.2876 2.2447 2.2240 2.1621 2.1027 2.0742

2.2320 2.2405 2.2451 2.2271 2.1813 2.1788

2.2192 2.2068 2.2113 2.1881 2.1675 2.1631

Further reading: Element-by-element operations in GAUSS (YouTube)

Step Three: Compute the Principal Components#

Now we will compute the estimated covariance matrix of our normalized yield variables and compute the eigenvalues and eigenvectors.

// Estimate the sample covariance matrix

yields_cov = varCovXS(yields_norm);

// Compute eigenvalues and eigenvectors

// of the covariance matrix

{ latent, coeff } = eighv(yields_cov);

print "latent = " latent;

print "coeff = " coeff;

latent =

0.0001

0.0003

0.0019

0.0104

0.1955

5.7918

coeff =

0.2371 -0.3070 0.5395 0.4677 -0.4165 0.4078

-0.6021 0.5065 -0.1919 0.1540 -0.3910 0.4092

0.5424 -0.0821 -0.6255 -0.2281 -0.2938 0.4117

-0.4177 -0.5250 0.1519 -0.5890 0.0903 0.4144

0.3246 0.5804 0.4139 -0.2970 0.3609 0.4099

-0.0848 -0.1732 -0.2943 0.5200 0.6700 0.3962

Function reference: eighv(), varcovxs()

Step Four: Rearrange and Interpret#

The eigenvalues and the corresponding columns of the eigenvector matrix are ordered from smallest to largest. We will reverse the order of the eigenvalues with the GAUSS rev function. Then we will reorder the columns of the eigenvector matrix.

// Reverse the order of the eigenvalues

latent = rev(latent);

// Create the sequence 6, 5, 4,...1

rev_idx = seqa(cols(coeff), -1, cols(coeff));

coeff = coeff[., rev_idx];

print latent;

print coeff;

5.7918

0.1955

0.0104

0.0019

0.0003

0.0001

0.4078 -0.4165 0.4677 0.5395 -0.3070 0.2371

0.4092 -0.3910 0.1540 -0.1919 0.5065 -0.6021

0.4117 -0.2938 -0.2281 -0.6255 -0.0821 0.5424

0.4144 0.0903 -0.5890 0.1519 -0.5250 -0.4177

0.4099 0.3609 -0.2970 0.4139 0.5804 0.3246

0.3962 0.6700 0.5200 -0.2943 -0.1732 -0.0848

Each column of the eigenvector matrix is a different component vector. The elements in the rows of these vectors contain the weights for the corresponding variables. To make intepretation more clear, we will transpose the eigenvector matrix and add the variable names to the columns.

headers = getcolnames(yields);

coeff = setcolnames(coeff', headers);

print coeff;

GS3M GS6M GS1 GS3 GS5 GS10

0.4078 0.4092 0.4117 0.4144 0.4099 0.3962

-0.4165 -0.3910 -0.2938 0.0903 0.3609 0.6700

0.4677 0.1540 -0.2281 -0.5890 -0.2970 0.5200

0.5395 -0.1919 -0.6255 0.1519 0.4139 -0.2943

-0.3070 0.5065 -0.0821 -0.5250 0.5804 -0.1732

0.2371 -0.6021 0.5424 -0.4177 0.3246 -0.0848

Function reference: cols(), getcolnames(), rev(), seqa(), setcolnames()

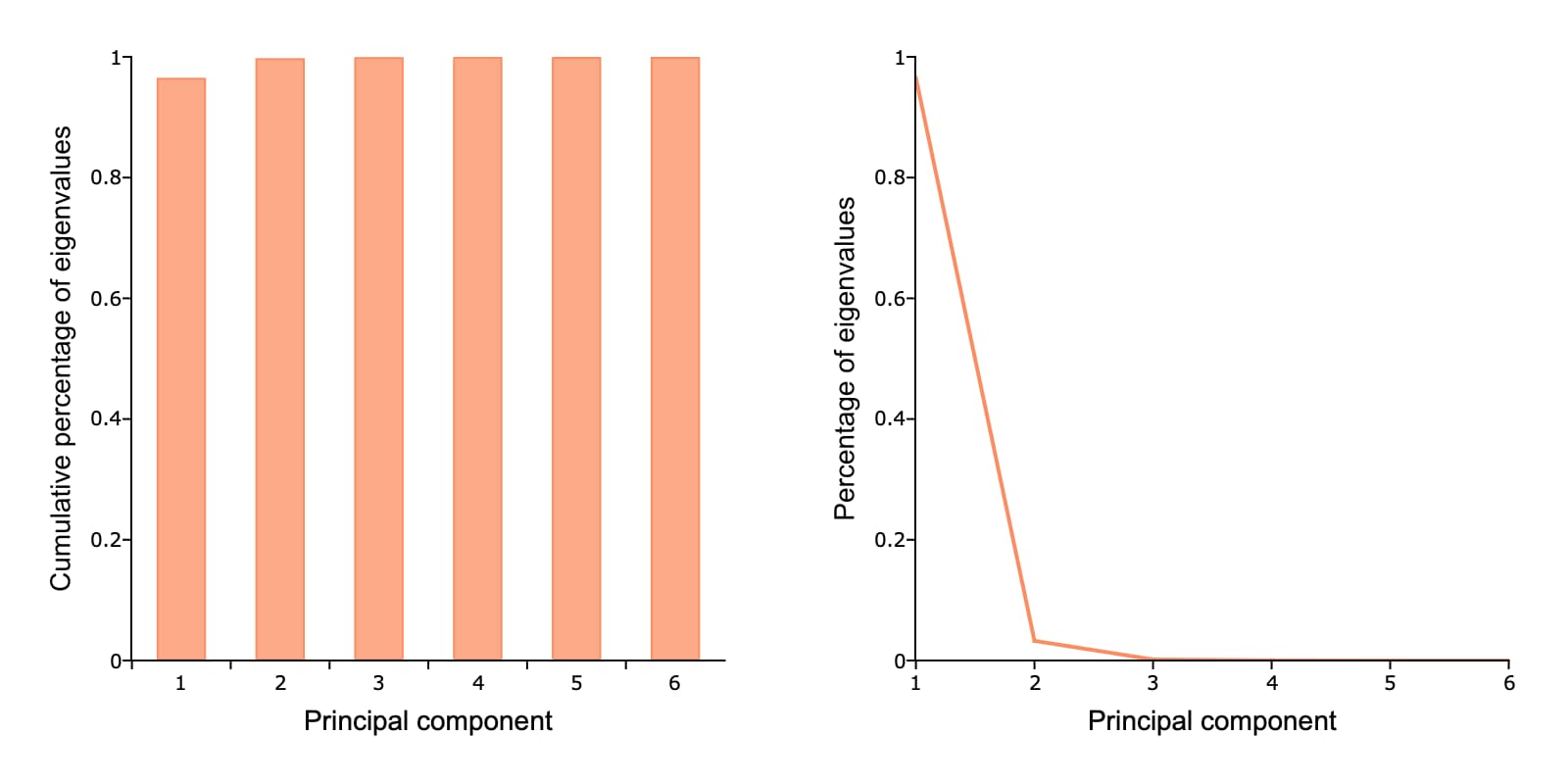

Step Five: Compute the variance explained#

We can compute the percent and cumulative percent of variance explained like this:

perc_lat = latent ./ sumc(latent);

cum_perc_lat = cumsumc(latent) ./ sumc(latent);

perc_lat = 0.965297 cum_perc_lat = 0.965297

0.032580 0.997876

0.001738 0.999614

0.000310 0.999924

0.000051 0.999976

0.000024 1.000000

To make interpretation even more clear, we will add the perc_lat variable to the front of the eigenvector matrix.

// Convert 'perc_lat' to be a dataframe

// with the column name 'VARIANCE'

variance = asdf(perc_lat, "VARIANCE");

// Use the horizontal contatenation operator

// '~' to add variance to the front of coeff

coeff = variance ~ coeff;

print coeff;

VARIANCE GS3M GS6M GS1 GS3 GS5 GS10

0.9653 0.4078 0.4092 0.4117 0.4144 0.4099 0.3962

0.0326 -0.4165 -0.3910 -0.2938 0.0903 0.3609 0.6700

0.0017 0.4677 0.1540 -0.2281 -0.5890 -0.2970 0.5200

0.0003 0.5395 -0.1919 -0.6255 0.1519 0.4139 -0.2943

0.0001 -0.3070 0.5065 -0.0821 -0.5250 0.5804 -0.1732

0.0000 0.2371 -0.6021 0.5424 -0.4177 0.3246 -0.0848

Step Six: Plot the results#

Finally we will plot the explained variance for each principal component.

// Set total size for both graphic panels

plotCanvasSize("px", 800|400);

// Declare 'plt' to be a plotControl structure

struct plotControl plt;

// Create the series 1, 2, 3,...6

component_idx = seqa(1, 1, rows(perc_lat));

// Split the graph canvas into a 1x2 grid and

// place the next graph in the first location

plotLayout(1,2,1);

// Fill the plotControl structure with default values

plt = plotGetDefaults("bar");

plotSetYLabel(&plt, "Cumulative percentage of eigenvalues", "arial", 14);

plotSetXLabel(&plt, "Principal component");

plotBar(plt, component_idx, cum_perc_lat);

// Split the graph canvas into a 1x2 grid and

// place the next graph in the second location

plotLayout(1,2,2);

plt = plotGetDefaults("xy");

plotSetYLabel(&plt, "Percentage of eigenvalues", "arial", 14);

plotSetXLabel(&plt, "Principal component");

// Fill the plotControl structure with default values

plotXY(plt, component_idx, perc_lat);

Function reference: plotbar(), plotcanvassize(), plotgetdefaults(), plotlayout(), plotsetxlabel(), plotsetylabel(), plotxy()

Further reading: