Introduction to GAUSS for R Users#

This guide assumes you know R and shows you how to do the same things in GAUSS.

Note

This guide is written for GAUSS 26.

How GAUSS Differs from R#

Core statistics are built in: OLS, GLM, quantile regression, optimization, plotting, and file I/O ship with base GAUSS. No

install.packages(), no dependency conflicts. Time series methods (ARIMA, VAR, GARCH) are available as add-ons.Dataframes are matrices: Named columns and typed variables, but you can do matrix algebra on them directly – no

as.matrix()conversion step. String columns are stored as integers with a lookup table, so they participate in matrix operations too.Columns are variables: Statistical functions operate on columns by default. R’s

colMeans(X)ismeanc(X),apply(X, 2, sd)isstdc(X),colSums(X)issumc(X).Results come back in structures: Estimation output is a structure with named members (

out.b,out.stderr), similar to R’s named lists.

Where to type code:

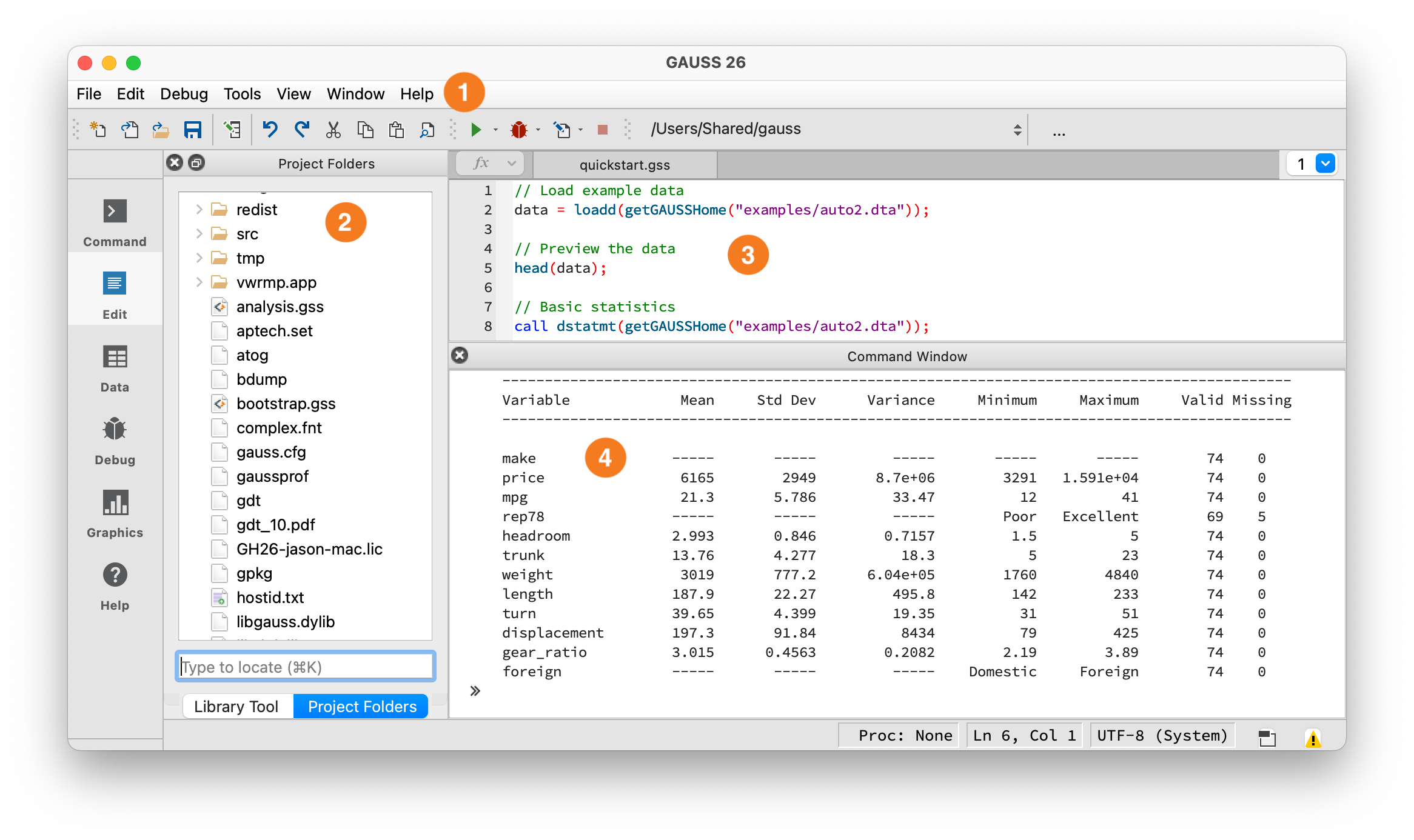

The GAUSS IDE workspace.#

① Toolbar — Shows your current working directory and the Run button (green arrow). Click it or press F5 to execute. ② Project Folders — File browser, similar to RStudio’s Files pane. ③ Editor — Write programs here, similar to RStudio’s Source pane. ④ Command Window — Output appears here, similar to the R Console. You can also type single lines at the >> prompt.

Debugging: Errors appear in the Output window with a line number – click it to jump to the error. Use the Variables panel (View > Variables) to inspect values at runtime. You can set breakpoints by clicking in the left margin of the editor, then step through code with the Debug menu. For quick debugging, insert print varname; statements.

Inspecting structures: To see what fields an output structure contains, use print – for example, print out; displays all members and their values. To see just the field names, check the structure definition in the Command Reference (press F1 on the function name).

Key Syntax Differences#

Feature |

R |

GAUSS |

|---|---|---|

Indexing |

1-based |

1-based (same) |

Assignment |

|

|

Matrix delimiter |

|

|

String quotes |

|

|

Statement end |

Optional |

Required |

All rows/cols |

leave blank or |

|

String concat |

|

|

Pipe |

|

None (use intermediate variables) |

Operators#

Arithmetic operators:

# R

A %*% B # Matrix multiplication

A * B # Element-wise multiplication

t(A) # Transpose

// GAUSS

A * B; // Matrix multiplication (R uses %*%)

A .* B; // Element-wise multiplication (R uses *)

A'; // Transpose

Warning

Operators are reversed! R’s * is element-wise; GAUSS’s * is matrix multiplication. R’s %*% is matrix multiply; GAUSS uses plain *. This will produce wrong results silently if you forget.

GAUSS has two forms of comparison operators. Without a dot, A > 0 returns a scalar – like R’s all(A > 0). With a dot, A .> 0 returns an element-wise result – like R’s A > 0:

# R

A > 0 # Element-wise comparison

A == B # Element-wise equality

A != B # Element-wise not-equal

A & B # Element-wise AND

A | B # Element-wise OR

// GAUSS

A .> 0; // Element-wise comparison (like R's A > 0)

A .== B; // Element-wise equality

A .!= B; // Element-wise not-equal (.ne also works)

A .and B; // Element-wise AND

A .or B; // Element-wise OR

Warning

Two forms of comparison. A > 0 returns a scalar (1 if all elements satisfy the condition) – equivalent to R’s all(A > 0). A .> 0 returns an element-wise vector – equivalent to R’s A > 0. Both forms exist for all comparison operators: >/.>, </.<, >=/.>=, <=/.<=, ==/.==, !=/.!=.

Warning

R’s ``|`` is OR. GAUSS’s ``|`` is vertical concatenation. Writing condition1 | condition2 in GAUSS does NOT give you logical OR – it stacks the two vectors vertically. Use .or for element-wise OR and .and for element-wise AND. This will silently produce wrong results, not an error.

Concatenation#

# R

cbind(A, B) # Horizontal (column bind)

rbind(A, B) # Vertical (row bind)

paste(a, b) # String concatenation

// GAUSS

A ~ B; // Horizontal concatenation (tilde)

A | B; // Vertical concatenation (pipe)

a $+ b; // String concatenation

For string arrays, use $~ (horizontal) and $| (vertical): "Domestic" $| "Foreign" creates a 2x1 string array.

Note

Most examples below use the auto2 dataset bundled with GAUSS. To run them, load it first:

auto2 = loadd(getGAUSSHome("examples/auto2.dta"));

Data Frames#

R’s data.frame and GAUSS dataframes are similar – tabular data with named columns of different types.

Creating:

# R

df <- data.frame(

name = c("Alice", "Bob", "Charlie"),

age = c(25, 30, 35),

score = c(85.5, 92.0, 78.5)

)

// GAUSS

name = "Alice" $| "Bob" $| "Charlie";

age = { 25, 30, 35 };

score = { 85.5, 92.0, 78.5 };

// Build a dataframe by concatenating single-column dataframes

df = asDF(name, "name") ~ asDF(age, "age") ~ asDF(score, "score");

Loading data: GAUSS’s loadd() reads CSV, Excel, Stata, SAS, SPSS, and HDF5 files – see Data Import/Export below.

Viewing:

# R

head(df)

str(df)

names(df)

nrow(df); ncol(df)

// GAUSS

head(df); // First 5 rows (same as R)

print df[1:6, .]; // First 6 rows (manual)

print rows(df) cols(df); // Dimensions

print getcolnames(df)'; // Column names (transposed for horizontal display)

getGAUSSHome() returns the path to GAUSS’s installation directory. Use it to access bundled datasets: loadd(getGAUSSHome("examples/auto2.dta")).

Column and Row Selection#

# R

df$price # Column by name

df[, "price"] # Column by name

df[, 3] # Column by position

df[, c("a", "b")] # Multiple columns

// GAUSS

df[., "price"]; // Column by name (dot = all rows)

df[., "price"]; // Same

df[., 3]; // Column by position

df[., "a" "b"]; // Multiple columns (space-separated names)

# R

df[1:5, ] # First 5 rows

df[df$age > 30, ] # Filter by condition

df[c(1, 3, 5), ] # Specific rows

// GAUSS

df[1:5, .]; // First 5 rows

selif(df, df[., "age"] .> 30); // Filter by condition (use selif, not brackets)

df[1|3|5, .]; // Specific rows (| concatenates index values)

Warning

GAUSS does not support boolean indexing in brackets. In R, df[condition, ] filters rows using a logical vector. In GAUSS, you must use selif(): selif(df, condition). Passing a boolean vector to brackets will not filter – it will try to use the 0s and 1s as row numbers.

Key difference: R uses blank or , for “all”, GAUSS uses . (dot). R’s df$col becomes df[., "col"].

Data Manipulation#

No pipes – use intermediate variables. R users chain operations with %>% or |>. GAUSS has no pipe operator. Store intermediate results in variables:

# R (tidyverse)

result <- auto2 %>%

filter(foreign == 0) %>%

mutate(price_k = price / 1000) %>%

arrange(mpg) %>%

select(mpg, price_k, weight)

// GAUSS -- same workflow, intermediate variables

domestic = selif(auto2, auto2[., "foreign"] .== 0);

domestic = dfaddcol(domestic, "price_k", domestic[., "price"] ./ 1000);

domestic = sortc(domestic, "mpg");

result = domestic[., "mpg" "price_k" "weight"];

Tidyverse verb mapping:

R (dplyr) |

GAUSS |

|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Data Import/Export#

# R

df <- read.csv("file.csv")

df <- haven::read_dta("file.dta")

df <- haven::read_sas("file.sas7bdat")

write.csv(df, "output.csv")

// GAUSS - one function reads everything

data = loadd("file.csv");

data = loadd("file.dta"); // Stata

data = loadd("file.sas7bdat"); // SAS

data = loadd("file.xlsx"); // Excel

// Load specific variables with a formula string

data = loadd("auto2.dta", "mpg + rep78 + price");

// Load all variables except one

data = loadd("auto2.dta", ". -rep78");

// Export

saved(data, "output.csv");

saved(data, "output.xlsx");

Formula string quick reference: GAUSS uses formula strings in several contexts with different syntax:

Context |

Example |

Separator |

|---|---|---|

|

|

|

|

|

|

Bracket indexing |

|

Space separates names |

Type overrides |

|

Keywords wrap variable names |

Note

GAUSS formula strings are quoted strings ("y ~ x1 + x2"), not bare expressions like R formulas (y ~ x1 + x2). The ~ separator works the same way in model formulas, but + in loadd() means “include this variable,” not “add to model.”

Missing Values#

R uses NA; GAUSS uses . (dot).

# R

is.na(x) # Element-wise check

any(is.na(x)) # Any missing?

na.omit(df) # Drop rows with any NA

x[!is.na(x)] # Keep non-missing

x[is.na(x)] <- 0 # Replace NA with 0

// GAUSS

x .== miss(); // Element-wise check (returns 1/0 vector)

ismiss(x); // Any missing? (returns scalar 1 or 0)

packr(df); // Drop rows with any missing value

selif(x, x .!= miss()); // Keep non-missing

missrv(x, 0); // Replace missing with 0

Warning

ismiss is NOT element-wise. R’s is.na(x) returns a vector. GAUSS’s ismiss(x) returns a scalar (1 if any element is missing, 0 otherwise). For element-wise missing detection, use x .== miss().

Statistics#

# R

mean(x)

sd(x)

sum(x)

min(x); max(x)

median(x)

var(x)

cor(x, y)

// GAUSS

meanc(x); // Column mean (the 'c' suffix = column-wise)

stdc(x); // Column std dev

sumc(x); // Column sum

minc(x); // Column min

maxc(x); // Column max

median(x); // Median

stdc(x)^2; // Column variance (scalar, like R's var(x) for a vector)

vcx(x); // Full variance-covariance matrix (like R's cov(X) for a matrix)

Correlation:

# R

cor(x, y) # Scalar correlation

cor(X) # Correlation matrix of all columns

// GAUSS

corrx(x ~ y); // 2x2 correlation matrix (~ is horizontal concat here, not a formula)

corrx(X); // Full correlation matrix of all columns

Note

Unlike R’s cor(x, y) which returns a scalar, corrx() always returns a matrix. To get a single correlation coefficient: corrx(x ~ y)[1, 2].

Linear Regression#

# R

model <- lm(price ~ mpg + weight, data = auto2)

summary(model)

// GAUSS - print formatted summary (like summary(model) in R)

call olsmt(auto2, "price ~ mpg + weight");

Tip

Use call olsmt(...) (with call) to print a formatted summary table to the screen without saving results to a variable. This is the GAUSS equivalent of summary(lm(...)). The call keyword discards return values.

Accessing results:

# R

coef(model)

summary(model)$coefficients[, "Std. Error"]

summary(model)$r.squared

residuals(model)

vcov(model)

// GAUSS

struct olsmtOut out;

out = olsmt(auto2, "price ~ mpg + weight");

print out.b; // Coefficient estimates (like coef(model))

print out.stderr; // Standard errors

print out.rsq; // R-squared

print out.resid; // Residuals

print out.vc; // Variance-covariance of estimates (like vcov(model))

Key olsmtOut members: b (coefficients), stderr (standard errors), vc (variance-covariance matrix), rsq (R-squared), resid (residuals), dwstat (Durbin-Watson), sigma (residual std dev), stb (standardized coefficients). To compute t-statistics and p-values: t = out.b ./ out.stderr. See the olsmt() reference for the full list.

For robust or clustered standard errors, pass an olsmtControl structure – see the olsmt() reference for details.

Logistic regression (GLM):

# R

model <- glm(admit ~ gre + gpa + rank, data = df, family = binomial)

// GAUSS

struct glmOut out;

out = glm(data, "admit ~ gre + gpa + rank", "binomial");

Quantile regression:

# R

library(quantreg)

rq(y ~ x1 + x2, data = df, tau = c(0.25, 0.5, 0.75))

// GAUSS (no package install needed)

struct qfitOut out;

out = quantileFit(data, "y ~ x1 + x2", 0.25 | 0.5 | 0.75); // | builds a vector

Plotting#

R users expect rich plotting. GAUSS has a full graphics library:

# R (base)

plot(x, y)

hist(x, breaks = 20)

boxplot(value ~ group, data = df)

# R (ggplot2)

ggplot(df, aes(x, y)) + geom_point() + labs(title = "Title")

// GAUSS

plotXY(x, y);

plotScatter(x, y);

plotHist(x, 20);

plotBox(data, "value ~ group");

plotBar(labels, heights);

plotSurface(x, y, z);

Setting titles, labels, and legends uses a plotControl structure. Think of it as GAUSS’s equivalent of ggplot’s + labs() + theme(), but configured before the plot call:

// Create a plot with title, labels, and legend

struct plotControl myPlot;

myPlot = plotGetDefaults("scatter");

plotSetTitle(&myPlot, "MPG vs Weight");

plotSetXLabel(&myPlot, "Weight (lbs)");

plotSetYLabel(&myPlot, "Miles per gallon");

plotSetLegend(&myPlot, "Domestic" $| "Foreign");

plotScatter(myPlot, auto2[., "weight"], auto2[., "mpg"]);

Subplots and saving:

# R

par(mfrow = c(2, 1)) # 2 rows, 1 column

ggsave("plot.png")

// GAUSS

plotLayout(2, 1, 1); // 2 rows, 1 col, position 1

plotSave("plot.png");

Linear Algebra#

# R

solve(A) # Inverse

det(A) # Determinant

eigen(A) # Eigenvalues and vectors

svd(A) # Singular value decomposition

chol(A) # Cholesky decomposition

qr.solve(A, b) # QR-based solve

solve(A, b) # Solve Ax = b

// GAUSS

inv(A);

invpd(A); // Inverse (positive definite, faster)

det(A);

eig(A); // Eigenvalues only

{ val, vec } = eigv(A); // Eigenvalues and vectors

{ u, s, v } = svdcusv(A);

chol(A);

olsqr(b, A); // QR-based solve (note: argument order is reversed from R)

b / A; // Solve Ax = b

Warning

eigv return order differs from R. R’s eigen(A) returns $vectors then $values. GAUSS’s { val, vec } = eigv(A) returns eigenvalues first, then eigenvectors. Swapping these produces wrong results silently.

Warning

``/`` is matrix division, not element-wise division. b / A solves the system Ax = b. For element-wise division, use ./. R’s / is always element-wise; GAUSS’s / is not.

Optimization#

R users doing custom MLE use optim(). GAUSS includes unconstrained and constrained optimization in the base package:

R |

GAUSS |

|---|---|

|

|

|

|

|

|

Key difference: R uses anonymous functions or named functions passed directly. GAUSS uses the & operator to pass a pointer to a named procedure. The & tells GAUSS to pass the procedure itself, not its result, so the optimizer can call it repeatedly with different parameter values:

# R

my_obj <- function(beta) {

resid <- Y - X %*% beta

return(sum(resid^2))

}

result <- optim(x0, my_obj)

// GAUSS -- named procedure; extra data passed as arguments

proc (1) = myObj(beta, Y, X);

local resid;

resid = Y - X * beta;

retp(resid'resid); // resid' * resid = sum of squared residuals

endp;

struct minimizeOut out;

out = minimize(&myObj, x0, Y, X);

For maximum likelihood estimation, see maxlikmt(), which provides a full MLE framework with standard errors, constraints, and convergence diagnostics.

Functions and Procedures#

# R

my_func <- function(x, y) {

result <- x + y

return(result)

}

// GAUSS

proc (1) = my_func(x, y);

local result;

result = x + y;

retp(result);

endp;

Key differences from R:

proc (n) =declares the number of return valueslocaldeclares variables scoped to this procedure (required – see warning below)retp()returns valuesendpends the procedureNo default argument values. All arguments are positional.

Multiple outputs:

# R

my_func <- function(x) list(a = x + 1, b = x - 1)

result <- my_func(5)

result$a; result$b

// GAUSS

proc (2) = my_func(x);

local a, b;

a = x + 1;

b = x - 1;

retp(a, b);

endp;

{ result_a, result_b } = my_func(5);

Warning

Variables are global by default. In R, function variables are automatically local. In GAUSS, you must declare them with local inside proc or they become globals that persist after the procedure returns. Forgetting local creates hard-to-find bugs where procedures silently read or modify variables from the calling scope.

Control Flow#

# R

for (i in 1:10) {

print(i)

}

if (x > 0) {

print("positive")

} else if (x < 0) {

print("negative")

} else {

print("zero")

}

while (x > 0) {

x <- x - 1

}

// GAUSS

for i (1, 10, 1);

print i;

endfor;

if x > 0;

print "positive";

elseif x < 0;

print "negative";

else;

print "zero";

endif;

do while x > 0;

x = x - 1;

endo;

Note: GAUSS requires semicolons after control statements (if, for, else, etc.). Inside a proc, remember to declare loop variables with local (see the warning above) or they become globals: local i; for i (1, 10, 1); ... endfor;

Common Function Translations#

Description |

R |

GAUSS |

|---|---|---|

Natural log |

|

|

Log base 10 |

|

|

Column mean |

|

|

Row mean |

|

|

Column sum |

|

|

Cumulative sum |

|

|

Sort by column |

|

|

Find indices |

|

|

Filter rows |

|

|

Remove missing rows |

|

|

Replace missing |

|

|

Check NaN (any) |

|

|

Check NaN (element) |

|

|

Flip rows |

|

|

Create diagonal matrix |

|

|

Full SVD |

|

|

Number to string |

|

|

String compare |

|

|

Formatted output |

|

|

Random uniform |

|

|

Random normal |

|

|

Set seed |

|

|

|

|

|

Comment |

|

|

Warning

log vs ln: In R, log is the natural logarithm. In GAUSS, log is base 10 and ln is natural. This will silently give wrong results if you don’t catch it.

R Package to GAUSS Mapping#

R assembles workflows from packages. GAUSS includes most of this in the base installation:

R Package |

GAUSS Equivalent |

|---|---|

|

Base GAUSS ( |

|

Base GAUSS ( |

|

Base GAUSS ( |

|

Base GAUSS ( |

|

Base GAUSS ( |

|

Base GAUSS ( |

|

TSMT add-on |

|

TSMT add-on |

|

TSMT add-on |

Time series users: If your work involves ARIMA, VAR, GARCH, impulse response functions, or forecasting, you will use the TSMT add-on. Key functions: arimaFit(), svarFit() (structural VAR), varmaFit(), varmaPredict(). For maximum likelihood estimation, see maxlikmt(). See the time series blog for complete worked examples.

Common Gotchas#

Semicolons are required. Every statement must end with

;Assignment uses ``=`` not ``<-``. GAUSS does not support

<-.Dot not colon for “all”. “All rows” is

df[., 1]notdf[, 1]. But:works for ranges:df[1:5, .].String quotes. Only double quotes

"string"work.No piping. No

%>%or|>– use intermediate variables or nested calls.The ``call`` keyword. Use

call functionName(...)to run a function and discard its return value. This is the GAUSS equivalent of runningsummary(lm(...))in R without assigning it.

For operator gotchas (* vs .*, | vs .or, dotted comparisons, log vs ln), variable scoping (local), boolean indexing (selif), and procedure ordering, see the inline warnings throughout this guide.

Putting It Together#

Here is a complete, runnable example that loads data, filters it, plots it, runs a regression, and prints the results. Running this prints the OLS summary to the Output window and opens a scatter plot.

// Load the auto2 dataset bundled with GAUSS

auto2 = loadd(getGAUSSHome("examples/auto2.dta"));

// Keep only domestic cars (foreign == 0)

domestic = selif(auto2, auto2[., "foreign"] .== 0);

// Quick scatter plot with title and labels

struct plotControl myPlot;

myPlot = plotGetDefaults("scatter");

plotSetTitle(&myPlot, "Weight vs MPG (Domestic Cars)");

plotSetXLabel(&myPlot, "Weight (lbs)");

plotSetYLabel(&myPlot, "Miles per gallon");

plotScatter(myPlot, domestic[., "weight"], domestic[., "mpg"]);

// Run OLS: how does weight affect fuel efficiency?

struct olsmtOut out;

out = olsmt(domestic, "mpg ~ weight");

// Print key results

print out.b; // Coefficient estimates

print out.stderr; // Standard errors

print out.rsq; // R-squared

What’s Next?#

GAUSS Quickstart – 10-minute introduction to GAUSS basics

Running Existing Code – If you inherited GAUSS code and need to get it running

Data Management – Loading, cleaning, and reshaping data

Textbook Examples – Worked examples from Greene (Econometric Analysis) and Brooks (Introductory Econometrics for Finance)

Command Reference – Browse all 1,000+ built-in functions

Econometrics blog – Fully worked examples covering regression, panel data, hypothesis testing, and more

Time series blog – ARIMA, VAR, GARCH, cointegration, and forecasting tutorials with complete code

See also

loadd(), olsmt(), glm(), quantileFit(), minimize(), plotXY(), packr(), selif()